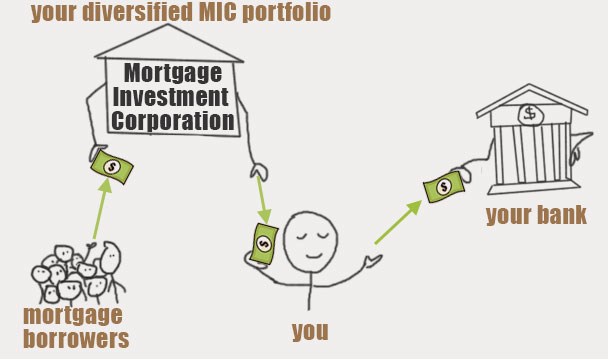

About Mortgage Investment Corporation

Appropriately, the goal is for investors to be able to access stable, long-term capital generated by a large resources base. Rewards obtained by investors of a MIC are normally categorized as rate of interest earnings for objectives of the ITA. Capital gains realized by a capitalist on the shares of a MIC are usually based on the normal treatment of resources gains under the ITA (i.e., in a lot of situations, taxed at one-half the price of tax obligation on common income).

While specific demands are loosened up till shortly after the end of the MIC's first financial year-end, the complying with requirements need to usually be pleased for a firm to certify for and keep its status as, a MIC: resident in Canada for purposes of the ITA and integrated under the legislations of Canada or a province (special rules apply to corporations included prior to June 18, 1971); just endeavor is investing of funds of the company and it does not handle or develop any real or unmovable property; none of the residential or commercial property of the corporation consists of financial debts possessing to the firm protected on genuine or immovable residential or commercial property located outside Canada, financial debts possessing to the company by non-resident persons, other than financial debts safeguarded on actual or unmovable property positioned in Canada, shares of the resources stock of corporations not homeowner in Canada, or genuine or stationary building positioned outside Canada, or any leasehold passion in such home; there are 20 or more investors of the corporation and no investor of the company (with each other with specific individuals connected to the shareholder) has, directly or indirectly, greater than 25% of the issued shares of any kind of class of the resources stock of the MIC (specific "look-through" guidelines use in respect of trust funds and partnerships); owners of preferred shares have a right, after settlement of preferred rewards and payment of rewards in a like quantity per share to the holders of the usual shares, to participant pari passu with the owners of common shares in any type of more dividend repayments; at the very least 50% of the expense quantity of all residential or commercial property of the firm is purchased: financial obligations safeguarded by mortgages, hypotecs or in any type of various other manner on "houses" (as specified in the National Real Estate Act) or on residential or commercial property consisted of within a "real estate project" (as defined read what he said in the National Housing Work as it continued reading June 16, 1999); deposits in the records of the majority of Canadian financial institutions or cooperative credit union; and money; the expense quantity to the firm of all real or immovable home, consisting of leasehold passions in such property (excluding specific amounts obtained by repossession or according to a borrower default) does not surpass 25% of the expense quantity of all its building; and it complies with the liability thresholds under the ITA.

The Ultimate Guide To Mortgage Investment Corporation

Capital Structure Private MICs usually provided 2 classes of shares, typical and favored. Typical shares are usually provided to MIC creators, directors and officers. Common Shares have ballot civil liberties, discover this info here are commonly not qualified to rewards and have no redemption function however join the distribution of MIC assets after chosen shareholders receive accumulated yet overdue rewards.

Preferred shares do not typically have ballot civil liberties, are redeemable at the alternative of the see this site owner, and in some instances, by the MIC. On winding up or liquidation of the MIC, preferred investors are commonly qualified to get the redemption value of each preferred share along with any type of declared yet unsettled dividends.

One of the most generally depended on prospectus exceptions for personal MICs distributing protections are the "certified investor" exemption (the ""), the "offering memorandum" exception (the "") and to a lower extent, the "family members, close friends and service partners" exception (the "") (Mortgage Investment Corporation). Capitalists under the AI Exception are generally higher web worth financiers than those who may just satisfy the limit to invest under the OM Exception (depending on the territory in Canada) and are likely to invest greater amounts of resources

Some Ideas on Mortgage Investment Corporation You Need To Know

Financiers under the OM Exception commonly have a lower total assets than recognized capitalists and depending on the jurisdiction in Canada go through caps appreciating the quantity of funding they can spend. In Ontario under the OM Exception an "qualified financier" is able to spend up to $30,000, or $100,000 if such financier gets viability recommendations from a registrant, whereas a "non-eligible capitalist" can just spend up to $10,000.

These structures promise stable returns at a lot greater yields than conventional set earnings investments nowadays. Dustin Van Der Hout and James Cost of Richardson GMP in Toronto believe so.